9559179325

9559179325 9559179325

9559179325 Login

Login

9559179325

9559179325

Overview of Insurance Company License

An insurance firm licence authorises a person to seek for and offer insurance products. The state insurance commissioner is in charge of issuing licences for the purpose of soliciting and selling insurance. These licences are divided into numerous insurance kinds, such as life and disability, health, auto, and worker's compensation. Anyone who lives in one state but sells insurance in neighbouring states must obtain a licence in each state. You do not need to work with an enlisted office to receive a licence, but it is essential if you wish to collaborate.

Prior to 1999, the Controller of Insurance was in charge of our country's insurance business, which was governed by the Insurance Act of 1938. However, the establishment of IRDA has resulted in considerable changes in the insurance industry. Individuals have been compelled to renew their insurance firm licences as a result of the IRDA's development. The insurance industry's previous provisions were out of date and irrelevant.

Before applying for any insurance company licence, all elements must get a Certificate from the Authority.The IRDA can provide permits for various types of insurance, such as life insurance, fire insurance, marine insurance, and so on. In any case, it is important to know that life insurance will not be combined with any other type of insurance.

IRDA's Purpose

The Insurance Regulatory and Development Authority of India (IRDAI) was established as a nodal organisation to oversee India's insurance industry. Aside from that, the agency keeps an eye on how insurance companies are regulated in India. This regulator guarantees that the relationship between insurance companies and policyholders remains balanced. Because your company will be dealing with financial products, obtaining an insurance licence is essential. Insurance contracts are agreements that guarantee the policyholder's financial protection in the case of a specific occurrence. As a result, these locations are regularly regulated. As a result, obtaining an IRDA licence is required before starting an insurance firm.

- The planning of the action of obtaining an insurance licence from the IRDA.

- The process of obtaining IRDA clearance for insurance items.

- The procedure for selecting an insurance intermediary.

Is it necessary to have an IRDA licence?

For the following reasons, an IRDA licence would be required:

- Ascertain that the insurance business complies with the IRDAI's laws and regulations as they are amended from time to time.

- Controlling the insurance industry in India. To preserve consumers' interests, the insurance industry must be carefully regulated.

- It also guarantees the public and authorities that proper norms and regulations are followed, as well as extra care and protection, when conducting insurance business.

- The IRDAI ensures that the insurance industry is constantly reviewed and regulated.

- The IRDAI will also deal with any policyholder complaints.

- As a grievance management mechanism, this would be addressed.

- Obtaining an insurance licence ensures that a company is in compliance with all insurance rules.

As a result, an IRDA licence is essential before launching an insurance firm in India for the reasons stated above.

Who is in charge of IRDA licencing?

The following is the key regulatory authority and the law that governs insurance (IRDA Licence):

- IRDAI- Insurance Regulatory Development Authority of India.

- Companies Act 2013 (the Companies Act)/ Companies Act 1956.

- IRDA (Registration of Indian Insurance Companies) Regulations 2000 (the Registration Regulations).

- IRDAI (Re-insurance) Regulations 2018 (Reinsurance Regulations).

- Any other relevant regulations which apply to securing an Insurance Licence in India.

Eligibility criteria for obtaining an IRDA License/Insurance Business License

The applicant must verify that the promoter or company meets the following criteria:

- To start an insurance company, you'll need 100 crores of cash, and to build a reinsurance company, you'll need 200 crores.

- As a result, for an insurance business, the applicant must have a minimum subscription capital paid-up value of 100 crores, and for a reinsurance business, it must have a minimum subscription capital paid-up value of 200 crores.

- Aside from that, the applicant must ensure that no previous application for founding an insurance company has been denied.

- • If a foreign firm or a non-resident Indian makes an equity investment, the foreign company or non-resident Indian must own 26 percent of the stock.

- If a bank wants to lau an insurance company, it must first obtain authorization from the Reserve Bank of India.

- An application to form an insurance company has not been denied in the recent five years.

- The IRDAI has not terminated or revoked the certificate.

- The company's name must include the term "insurance company."

Other requirements for beginning a business in the insurance industry include:

Documents Required for Insurance Company License

To get an insurance company licence, a candidate must submit an application to the IRDAI in the form IRDAI/R1 for the issuing of a demand for the registration application. The following documents will be used to support the application:

- Applicant is a business entity established under the Companies Act of 2013.

- MOA and AOA certifications.

- Names, addresses, and occupations of the directors are provided.

- For the previous five years, a certified copy of the annual report of Indian promoters and international investors.

- Certified copy of the applicant's shareholding agreement with Indian promoters and foreign investors.

- The Board of Directors approved a five-year business plan.

Application for Insurance Company License Registration

The candidate will apply in Form IRDAI/R2 for the issuing of a certificate of registration once the authority has acknowledged the application for demand.

The following information will be included in the application:

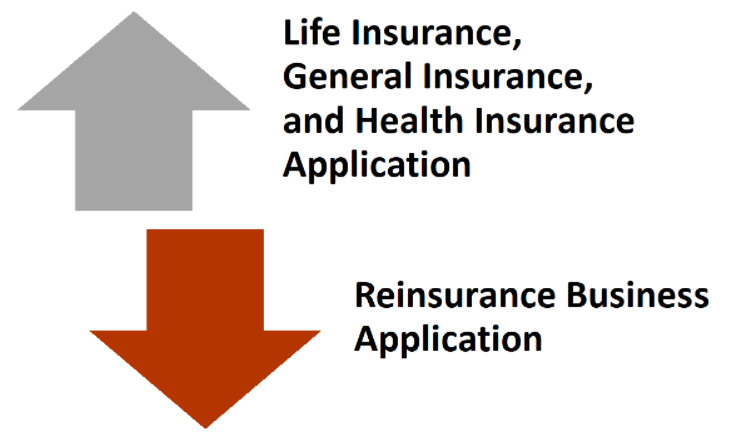

Life Insurance, General Insurance, and Health Insurance Application

Evidence demonstrating that the settled-up value capital is greater than or equal to Rs. 100 crores.

Reinsurance Business Application

The evidence indicates that the settled-up value capital is greater than or equal to Rs. 200 crores.

- An affidavit signed by the Indian and foreign promoters attesting to the fact that the paid-up equity capital is sufficient after deducting preliminary costs.

- Shareholding articulation that includes the unique number of shares given to promoters.

- The holding of remote paid-up equity capital is computed as mentioned under the Indian Insurance Companies (Foreign Investment) Rules, 2015 read with distinct principles identified with it, according to the CEO, MD, WTD of Indian developers and foreign investors.

- If FDI exceeds the 26 percent limit, the FIPB must approve it.

- A certified copy of a prospectus that has been published.

- A certified copy of the Memorandum of Understanding (MOU) or any other agreement between the promoters, such as a management agreement, a shareholder agreement, a voting agreement, or any other arrangement.

- Confirmation of the non-refundable payment of Rs. 5 lakh in costs.

- PCA or PCS certificate confirming the registration charges, value share capital, and other Act needs are all in order.

Following receipt of the application, the authority will consider the type of the insurance products, the level of actuarial, bookkeeping, and other specialised specialists in the administration, and the organisation structure.

After performing an investigation and being satisfied, the authorities will award the applicant a certificate in Form IRDAI/R£. If the Authority is not satisfied with the information provided by the candidate for the purpose of obtaining an insurance company licence, the application may be dismissed.

The candidate shall be notified of their rejection within thirty days of the date on which the order of rejection was issued, along with the reason for rejection. Within 30 days of receiving the discharge order, a candidate can speak with SAT.

The candidate who has earned an insurance company licence certificate must start doing business within 12 months of receiving the certificate.

Obtaining an Insurance Company License Registration Procedure

- A candidate can submit an application for additional security, a general insurance company, a health insurance company, or a reinsurance company.

- After accepting an application, the Authority may request more information or explanations related to the application.

- Following completion, the Authority may grant approval, and the candidate must then submit a new application in Form IRDAI/R2 for the issue of a certificate of registration.

- By documenting the reason as a hard copy, the Authority may dismiss the application for issue of an order for a registration form.

- A candidate who has been mistreated by the decision must file an appeal with the Securities Appellate Tribunal within 30 days after receiving the dismissal letter.

Circumstances under which an applicant is unable to file an IRDAI/R1 application

- If the authority has refused your registration request.

- If any international or Indian investors decide to withdraw from the project for whatever reason.

- Time from the date of the requisition for registration application throughout the previous two financial years.

- During the previous two monetary years from the date of the order for registration application, the Authority has dismissed or pulled back the candidate's application for registration under any conditions.

- If your Certificate of Registration has been abandoned by the regulating authority.

- If the applicant's name does not contain the words "insurance" or "assurance," the application will be rejected.

Suspension of Certificate of Insurance Company License

- Failure to comply with the arrangements of the activities identified with the calculation of benefits and liabilities results in the suspension of the certificate of insurance company licence.

- The insurance is under liquidation or has been declared bankrupt.

- Without the Authority's consent, the guarantor's business or a class of the guarantor's business has been transferred to or amalgamated with the business of another safety net provider.

- Failure to comply with the terms of the Act, the Rules and Regulations, or the Authority's instruction or order.

- Any case that is unpaid for more than three months after the court's decision is rendered remains unpaid.

- Insurer conveys business that isn't related to insurance or that isn't advised.

- Failure to assent to the necessity of the Companies Act, 2013, the General Insurance Business Act, 1972, the Foreign Exchange Management Act, 1999, or the Money Laundering Prevention Act, 2002.

- Failure to pay the yearly costs imposed by the Act.

Insurance Licence Validity- IRDA Licence

For one year, an IRDA licence would be valid. In order to renew an insurance licence in India, the applicant must submit a new application.

Renewal of IRDA Licenses in India

An applicant with an insurance licence will use Form IRDA/ R5 to submit their application. This application must be submitted before the end of the calendar year. When submitting an application for renewal, the following documents must be submitted as proof of renewal:

- Each type of insurance costs 50,000 rupees.

- One-fifth of one percent of the total gross premiums collected by the insurance company during the financial year preceding the year in which the certificate must be renewed.

- Alternatively, Rs 5 crore, whichever is less.

If the insurance company does not renew before the 31st of December each year, the authority will accept the application. However, if payments are not paid on time, the applicant will be charged a penalty of 10% of the total fee due.

The fee will be deposited into the Insurance Regulatory and Development Authority of India's account with the Reserve Bank of India.

Duplicate Certificate

In addition, the IRDAI has the ability to provide a duplicate certificate to the insurance company. The applicant must file an IRDA/R4 application and pay a fee of Rs 5000/-.

Why Choose Us

Free Legal Advice

Transparent Pricing

On Time Delivery

Expert Team

Money Back Guarantee

200+ CA/CS Assisted

Lowest Fees

Easy EMIs

Frequently Asked Questions

When the authority receives the IRDA/R1 form and approves it, the applicant will be given the IRDA/R2 form. The applicant must submit IRDA/R2 to the authority once it has been completed. If the authorities approve IRDA/R3, the applicant can start his or her insurance company. However, the insurance business must begin within one year of the licence being granted.

All unforeseen risks will be covered by general insurance. Under general insurance, the following dangers would be covered: Accidents, Illness, Fire, Securities in the Financial Sector, Burglary & Property Loss. General Insurance will give you with much-needed protection in the event of such unforeseeable disasters. Unlike Life Insurance, General Insurance is designed to safeguard against unexpected events rather than provide a profit. Some types of insurance, such as motor insurance and public liability insurance, have been made mandatory by particular Acts of Parliament.