9559179325

9559179325 9559179325

9559179325 Login

Login

9559179325

9559179325

Overview of NBFC Collaboration

Collaboration refers to people working together toward a common purpose. India has over 9000 active NBFC licences, however only 954 of them have book sizes greater than 40 crores. The remaining 8046+ NBFCs can only fulfil the regulation loan book cap of INR 20 million. NBFC Collaboration is a new business phrase that refers to NBFC License holders forming partnerships with banks or Fintech firms to get leads and funds. Both parties may or may not share revenue and may or may not incur some level of NPA risk.

Traditional big size NBFCs have been suffering liquidity issues in 2019 due to strict RBI supervision, but mid-size and small size NBFCs have been doing well and have been able to attract a significant amount of FDI for retail lending.

In NBFC Collaborations, NBFCs with exposure to at least 20% of loan books must fund the remaining loan book amount with the Bank or Fintech Company at the agreed-upon interest rate. If there are innovative loan products and speedy loan disbursement using the latest technologies, NBFC collaboration is quite successful.

The NBFCs operating on a large scale suffered from the economic crisis in 2019 as a result of the Reserve Bank of India's tough governance standards. Medium- and small-scale NBFCs, on the other hand, have had a difficult time, although they have made headway and are now able to raise a sizable amount of FDI for retail lending. They are, without a doubt, becoming commercially successful. The partnership of large scale NBFCs with Fintech firms and banks is bringing the companies participating in all of these processes to their happiest days yet. Furthermore, the NBFC collaboration will aid in the discovery of new approaches to gain clients as well as the achievement of the primary goal, which is to raise capital.

Collaboration amongst NBFCs has its own set of dynamics. Let’s Understand!

NBFCs and banks are always attempting to address the population's and enterprises' financial demands. However, as the cost of money rises, NBFCs are focusing more on creating customised products to fulfil individual demands. Unlike banks, which are also regulated by the RBI, there are some distinctions between NBFCs and banks, which are stated below:

- Demand Deposits are not accepted by non-bank financial institutions (NBFIs).

- NBFCs are unable to issue checks.

- If you're looking for a way to insure your deposits, NBFCs aren't the place to go because they don't offer deposit insurance.

As a result, NBFCs must maintain constant efforts to secure their domain and build a loyal customer base. Advance salary loans, student loans, medical loans, travel loans, and other types of loans are among the numerous types of loans in which new-age NBFCs are involved. Big data and block chain technologies are proving to be stepping stones in alternative lending strategies, necessitating significant expenditures in technology and the loan origination process.

In India, NBFC Collaboration is a new idea in which NBFC licence holders work with growing Fintech firms. It's done to generate leads and make funding easier. The agreement is being created, and it outlines the basic terms, such as the income sharing plan between the two parties. It also shows the percentage of NPA and the danger it poses to both parties.

Large NBFCs are also experiencing liquidity issues, which can be ascribed to RBI regulations, but the situation for mid-size and small NBFCs is different because they are able to draw significant amounts of FDI, allowing them to pursue retail lending with ease. The increased use of mobile phones and smartphone penetration has prompted NBFCs to reach out to lower-income clients, using their cell phones for loan origination, e-KYC, and disbursement e-signature. By using Robotic Automation, operational workflows have been streamlined, productivity has grown, accuracy has increased, and cost savings have been maintained. NBFCs are also putting new age technologies like e-KYC, data exchange, loan disbursement and collection, and cyber security into action. For greater connectivity among all stakeholders, application programming interfaces (APIs) are being established and used.

FinTech’s are quickly advancing in the realm of acing technology, making Banks and NBFCs' overall responsibilities easier. Even if NBFCs try to construct their own automated system, their progress is poor because to their sluggish approach and reliance on old methods. As a result, fintech players step in to help. In the case of NBFC Collaboration, the normal exposure of 20% of the NBFC's loan books is visible, and the interest rate is determined by which Fintech business or bank funds the remaining loan book. The foundation of successful NBFC Collaboration is the development of novel loan products as well as effective loan disbursement using technology.

What are the advantages of collaborating with Fintech firms for NBFCs?

NBFCs are keeping a wary eye on Fintech Companies, and it's a truth that Fintech Companies are the next big thing, thus cooperating with them would yield surprising and remarkable consequences. NBFCs are emerging from the woods in order to expand their lending capacities. This relationship will help not only NBFCs, but also Fintech Companies, who will be able to dominate newcomers in the business after partnering with NBFCs. In a nutshell, we can say that it will be a win-win situation for them both.

The following are the advantages that NBFCs obtain from partnering with Fintech companies:

Increase your Productivity

The internal and external functions of NBFCs have been simplified thanks to fintech. It also aids the seamless operation of non-banking financial companies. Furthermore, it encourages NBFCs to update their back-office activities, resulting in increased efficiency.

Introducing New and Innovative Product Offerings

Non-Banking Financial Companies are bringing fresh modifications to their new offerings by utilising Fintech's latest technology-based capabilities. The combination of NBFCs and Fintech Players aids in the introduction of new and in-demand product offerings such as Payday Loans, POS Financing, Consumer Durable Loans, Invoice Financing, and other similar products.

Embracing Paperless and Digitally Modernized Modes

NBFCs become familiar with the extraordinary tactics after joining forces with a Fintech company. It persuades NBFC to use paperless digital ways rather than the old, inefficient manual approach. Most importantly, digital onboarding and verification reduces operational costs.

Is it necessary for an NBFC to look at the FLDG (First Loss Default Guarantee) or Fintech balance sheet?

The background of financial companies must be checked by the NBFC Company before it approves any collaboration. The NBFC company should conduct thorough research on the Fintech company and learn about the Fintech company's financial capacity. Furthermore, they must be aware of the promoters as well as facts on their profile. When dealing with overseas Fintech corporations, this information becomes much more critical. Conducting due diligence is a must-do task before signing any NBFC Collaboration agreement. Fintech enterprises must also adhere to the necessary regulations.

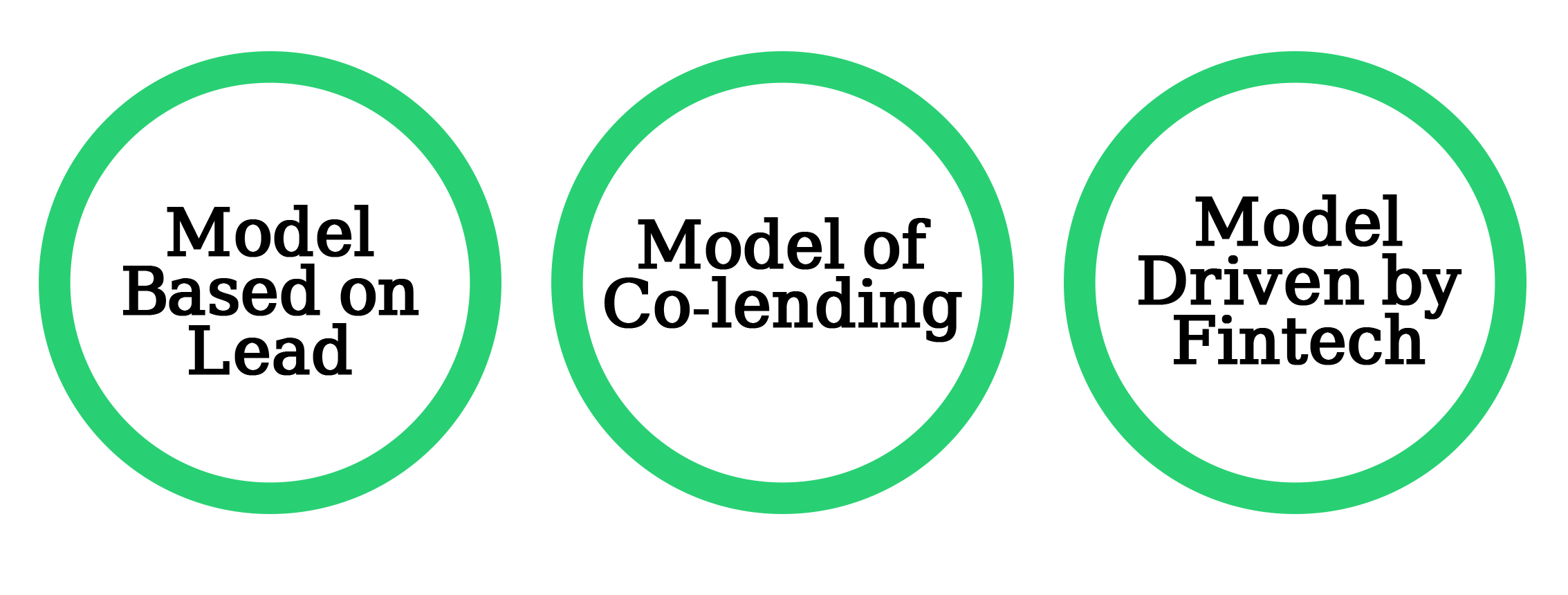

Model based on lead

Fintech Company provides cutting-edge and unique tech-driven underwriting and risk reduction by delivering risk assessment tools and services in this manner. The Fintech Company often receives a commission from the NBFC in the region of 1% to 3%.

Model of co-lending

The Fintech Company delivers the much-needed information and tools that help the Non-Banking Financial Company make quick loan processing choices. Fintech firms are implementing the First Loss Default Guarantee Model with the help of their dedicated Escrow Account. Fintech firms are likely to share their ROI with NBFCs, which ranges from 24 percent to 36 percent. Fintech companies do their job when it comes to covering 100% of NPA and expenditures.

Model Driven by Fintech

The First Loss Default Guarantee is a mechanism that protects the lender's interest in the NBFC. Lenders need collateral in order to secure their Fintech Company advances. It's a Fintech-Driven Approach.

Collaboration Business Model for NBFCs

Company (1)

Fintech companies would benefit greatly from online and offline marketing strategies in terms of generating leads. A Fintech company must be required to deposit sufficient funds with the fund management as FLDG. The fund management will deposit the money in a Non-Banking Financial Company as Inter-corporate deposits.

Company (2)

According to the Fintech Company's instructions, the funds will be managed by a consulting firm, a lawyer, or a CPA. Fintech Company will be charged a significant amount of service fees for their respective services.

Company (3)

The NBFC, which is regulated by the Reserve Bank, is in charge of loan distribution and underwriting. The Fintech Company will share a list of consumers who are interested in various loan products, and the NBFC will distribute funds after the risk assessment procedure is completed. NBFC will retain a portion of revenue after accounting for risk management services and services connected to loan management. The remaining profit will be divided with the Fintech Company.

Reason for Collaboration between a bank and a Non-Banking Financial Institution (NBFC)

The call for partnerships between an NBFC and a bank is something that requires everyone's attention, taking into account the general requirement to give credit, as well as ensuring the economic boost and development of the economy.

The following are the main reasons behind this collaboration.

- Ensure that the market has enough liquidity.

- Increasing the amount of credit available to debtors.

- Meet lending goals in key industries.

- Giving priority and other industries a boost.

- Expand your banking outreach.

- Avoid a liquidity constraint (Also known as credit crunch).

- Increase and improve financial inclusion.

Insights about the NBFC's Compliance Requirement

Some of the insights regarding NBFC Compliance requirement are as follows-

- The ID verification, Aadhaar verification, and PAN Card verification processes are all accomplished online.

- Maintain and store borrowers' data for a period of five years.

- Taking pictures of the borrowers in real time.

- Pay the E-stamp duty after the loan agreement is signed.

- The need is to report to credit information businesses in the event of a loan inquiry, delay, disbursement, or default.

- Comply with the Reserve Bank of India's CKYC guidelines.

- Follow the TDS, GST, RBI Act, and the Companies Act.

- Hire a CPA to control the hazards that come with running a business, and this can also help with a surprise check and inspection of the Fintech firm.

- Bring forth the provisions for NPA based on loan book performance requirements of 45 or 90 days.

Fintech Company's Minimum Desired Technology

Fintech Company's Minimum Desired Technology are as follows-

- In order to compete in the Indian market, you must have a mobile app.

- Systems such as a loan administration system, a loan origination system, and a collection system should be installed.

- Credit and underwriting software must be owned by a fintech company.

- Because it will protect the borrower's personal information, the Fintech Company must ensure that there is no lag in terms of IT security.

- The Loan App must be able to integrate a variety of APIs, including but not limited to PAN, Aadhaar, and Driver License.

- It needs to be able to verify the profiles of live borrowers.

- Checking the income process necessitates the analysis of bank statements.

- Borrowers' faces and the IDs they submit online must appear to be identical.

- Online verification of employment profile.

- In order to use social scoring technology, Indian law requires that privacy standards be followed.

- The server must be located in India and must not be located outside of India's borders.

India's Foreign Direct Investment (FDI) policy for Fintech Companies.

- According to one of the RBI's notifications, new rules require Fintech companies to accept 100 percent foreign direct investment via the automated channel.

- There is currently no regulation in place that specifies the minimum capital required for operating a Fintech business in India.

The Fintech Industry's Compliance Requirement

- Fintech Company has the capacity and right to grant loans or guarantees up to 60% of its paid-up capital and 100% of its free reserve plus security premium, whichever is greater, through board resolution.

- After the members have given their consent, the company can be allowed to use up to 100% of its paid-up capital.

- On loan processing costs, a fintech company should pay the Goods and Services Tax. Nonetheless, in normal practise, the processing charge is usually inclusive of GST.

- If foreign funds are raised as a loan or debt, the Fintech Company must follow ECB standards.

You can contact us if you have any questions or concerns about the NBFC Collaboration Model, or if you are waiting for the appropriate time to collaborate with NBFC. If you require any additional information from our end, we will be pleased to assist you. We will also give you necessary resources as soon as possible. BIZ Advisors will go to great lengths to ensure your complete satisfaction.

Process of Collaboration between an NBFC and a Fintech Company.

Collaboration between NBFCs and Fintech Firms is on the rise. Observe this Procedure-

- The co-origination plan agreement must be signed by both the NBFC and the Fintech company.

- A fund manager and a fintech company must agree to sign inter-corporate deposit agreements.

- The NBFC that is a part of the relationship should sign a platform service agreement that allows the Fintech business to be paid for its technology services.

- The NBFC will need to open a separate bank account to suit the loaning demands.

- The NBFC takes the initiative and opens an Escrow Account (a separate account for disbursement and re-payment purpose).

- Appoint a Chartered Accountant with extensive experience in maintaining and administering Escrow Bank Account funds and services.

- Following the start of operation, Fintech companies should carefully monitor and keep an eye on regular compliance (CKYC, TDS, GST, Credit Reporting, and others).

- Monthly reconciliation and Credit Information Company (CIC) reporting

- Following the 45 - 90-day NPA provisioning norms is a must for NBFCs to consider.

Why Choose Us

Free Legal Advice

Transparent Pricing

On Time Delivery

Expert Team

Money Back Guarantee

200+ CA/CS Assisted

Lowest Fees

Easy EMIs

Frequently Asked Questions

The numerous Fintech-NBFC collaboration models are as follows:

Fintech-Led Model; Lead-Based Model & Co-Lending Model.